Sunday, February 26, 2023

Friday, February 24, 2023

Thursday, February 23, 2023

Congratulations to the GDS candidates selected to departmental cadres ....

From Gudur dn total 11 members selected to departmental cadre

Postman cadre

1.N. Jhonsyrani, BPM Budanam Bo -- selected and allotted to Rajamundry Division

2.D. Jagadeeswari, BPM Kokkupadu. selected and allotted to Visakhapatnam division

3.Ch. Nagaraju selected and allotted to Rajamundry Division

4.I. Ramakrishna selected and allotted to Visakhapatnam division

5.K. Ramachandraiah BPM, Muttembaka selected and allotted to Visakhapatnam division

6.R. Suresh selected and allotted to Visakhapatnam division

1.K. Penchalamma BPM Utukuru selected and allotted to RMS 'Y' dn.

2 N. Rajasekhar selected and allotted to RMS 'Y' dn

3.K. Sarala selected and allotted to RMS 'V' dn

4.R. Sreenivasulu selected and allotted to RMS 'V' dn

1. K. Bunni Bhagyasri BPM Gulimcherla selected and allotted to Gudur division

Congratulations to all...

NFPE - GUDUR

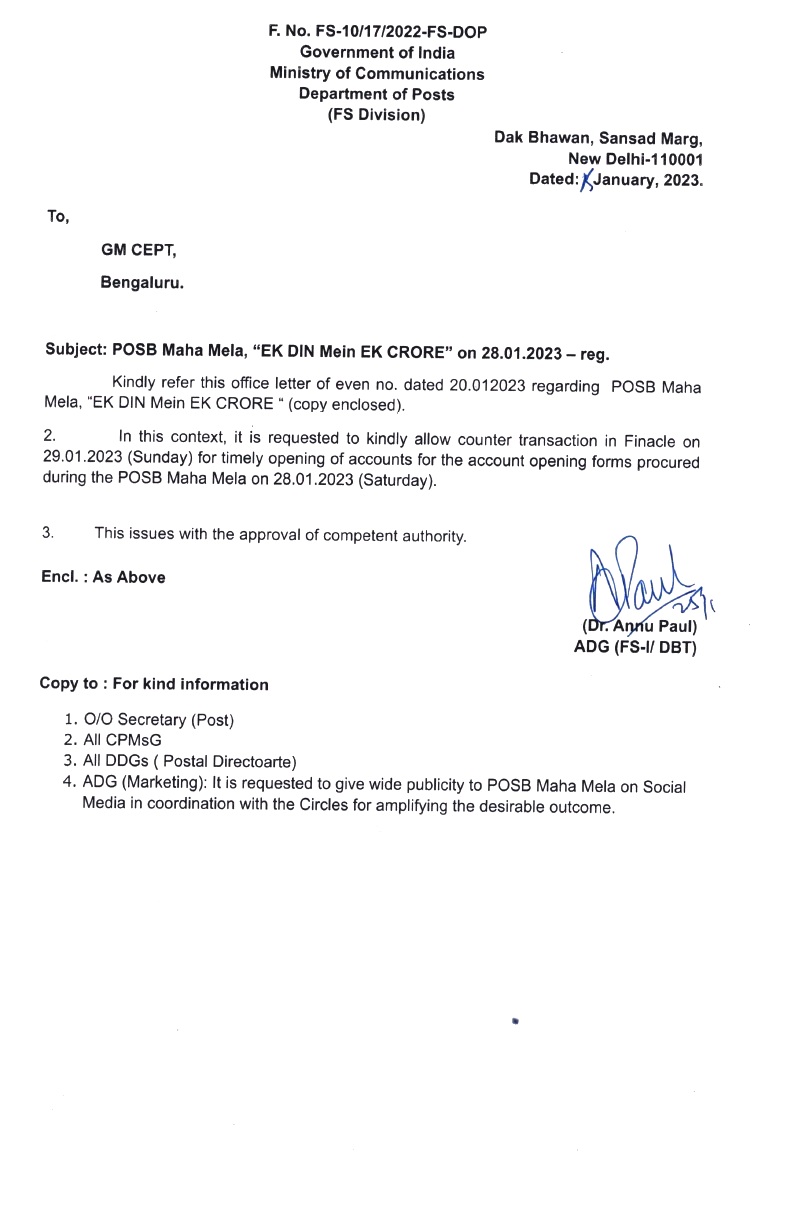

Wednesday, January 25, 2023

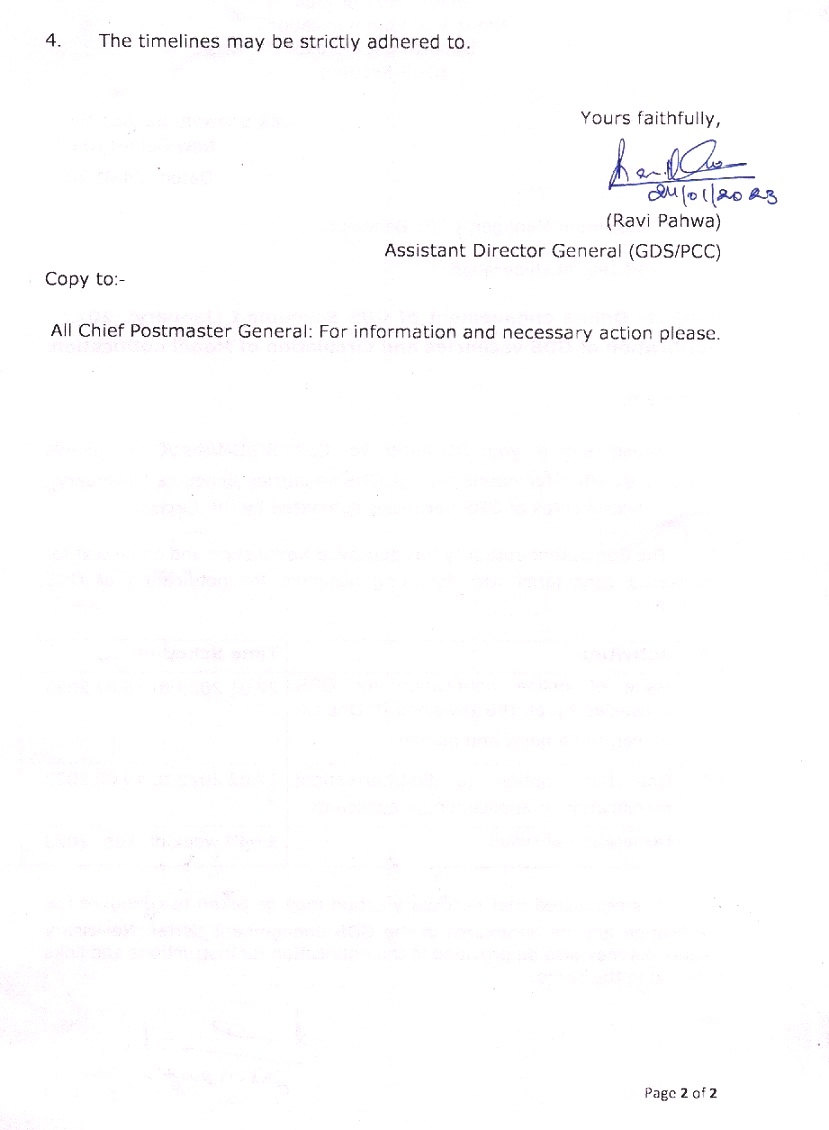

CEPT :: Maintenance of SAP from 26 Jan, 3 am to 27 Jan, 4 am

Gudur :: Today's Demonstration during lunch hour in front of Divisional Office (25-01-2023)

డియర్ కామ్రేడ్స్,

డిపార్ట్మెంట్ అవలంబిస్తున్న బలవంతపు టార్గెట్స్ కు నిరసనగా...28-01-2023 న దేశావ్యాప్తంగా కోటి అకౌంట్ లు ఓపెన్ చేయాలన్న సాధ్యం కాని టార్గెట్స్ మరియు పెండింగ్ లో ఉన్న TA bills వెంటనే ఫండ్స్ అలాట్ చేసి పాస్ చేయాలని, TA అడ్వాన్స్ సకాలంలో ఇవ్వాలని, GDS substitute శాలరీ payment చేయాలని, contingent వాళ్లకు allowances ఇవ్వాలని, NFPE అనేక సార్లు డిమాండ్ చేసిన problems సాల్వ్ చేయక పోవటం తో 25.01.2023 న దేశవ్యాప్తంగా లంచ్ hour ధర్నా కు పిలుపు ఇవ్వడం జరిగింది. దానిలో భాగంగా ఈరోజు ఉదయం 9-00 గూడూరు హెడ్ పోస్టుఆఫీస్ వద్ద ధర్నా ను నిరహీంచడం జరిగింది. కార్యక్రమం లో డివిజన్ నాయకులు కా" R. గోవింద నాయక్, C. సుధాకర్ రాజు, K. చంద్రశేఖర్, ch. v. రమణయ్య, A. మల్లిఖార్జున తదితరులు పాల్గొన్నారు.

Tuesday, January 24, 2023

Gudur Division :: Lunch Hour Demonstration on 25-01-2023 at the call of NFPE

NFPE - GUDUR

Wednesday, January 18, 2023

NFPE - GUDUR heartfully welcomes Com.Subbalakshmi, PA, Gudur HO ....

Model Notification :: Competitive Examination for recruitment to the cadre of Postal Assistants and Sorting Assistants from Gramin Dak Sevaks (GDSs) for the unfiIled Limited Department Competitive Examination vacancy of Postal Assistant and sorting Assistant of the year 2023 (01.01.2023 to 31.12.2023).......

Tuesday, January 17, 2023

Saturday, January 14, 2023

Seasonal & Festival greetings to all ........

మీకు మీ కుటుంబ సభ్యులకు భోగి శుభాకాంక్షలు

NFPE - GUDUR

Tuesday, January 10, 2023

GUDUR DIVISION :: 30th Biennial Divisional Conference held on 08-01-2023

The Conference inaugurated by Sri P.Syam Prasad Reddy garu, Chairman, Pernati Charitable Trust. Com.Janardhan Majumdar, Secretary General NFPE & General Secretary, AIPEU GrC., and Com. Tapan Bhowmik, General Secretary, AIPEUGDS attended as Chief guests and addressed the Conference.

Com.R.N.Sarat Kumar, Orgg. General Secretary, AIPEU GrC (CHQ) Com. B. Sridharbabu, Convener, C-o-C, NFPE, A.P Circle & Circle Secretary, Gr.C., Com.Y.V.Achyutkumar, Circle Secretary, AIPAOEU., Com.Ch.Vidyasagar, AGS (CHQ) & Circle Secretary, AIPEU PM&MTS.,Com.K.Murali, Circle President, P-4., Com. M. Srinivasarao, AGS (CHQ) & Circle Secretary, AIPEUGDS, Com.N.Nageswararao, Circle Secretary, AIPRPA., Com.M.Ramakrishna, ACS, Gr.C, A.P.Circle and many leaders of NFPE & AIPRPA attended and addressed the meeting.

Divisional Secretaries & Members of Nellore & Tirupati Divisions were also present.

During the sessions of Conference, Com.P.Pandurangarao, Ex-General Secretary, AIPEUGDS has been felicitated on his retirement on 05-01-2023.

The Conference organized by Com. K. Sudhakar, Ex-Divisional Secretary and their team with all decoration, warm reception, proceedings of the meeting deserves all appreciation.